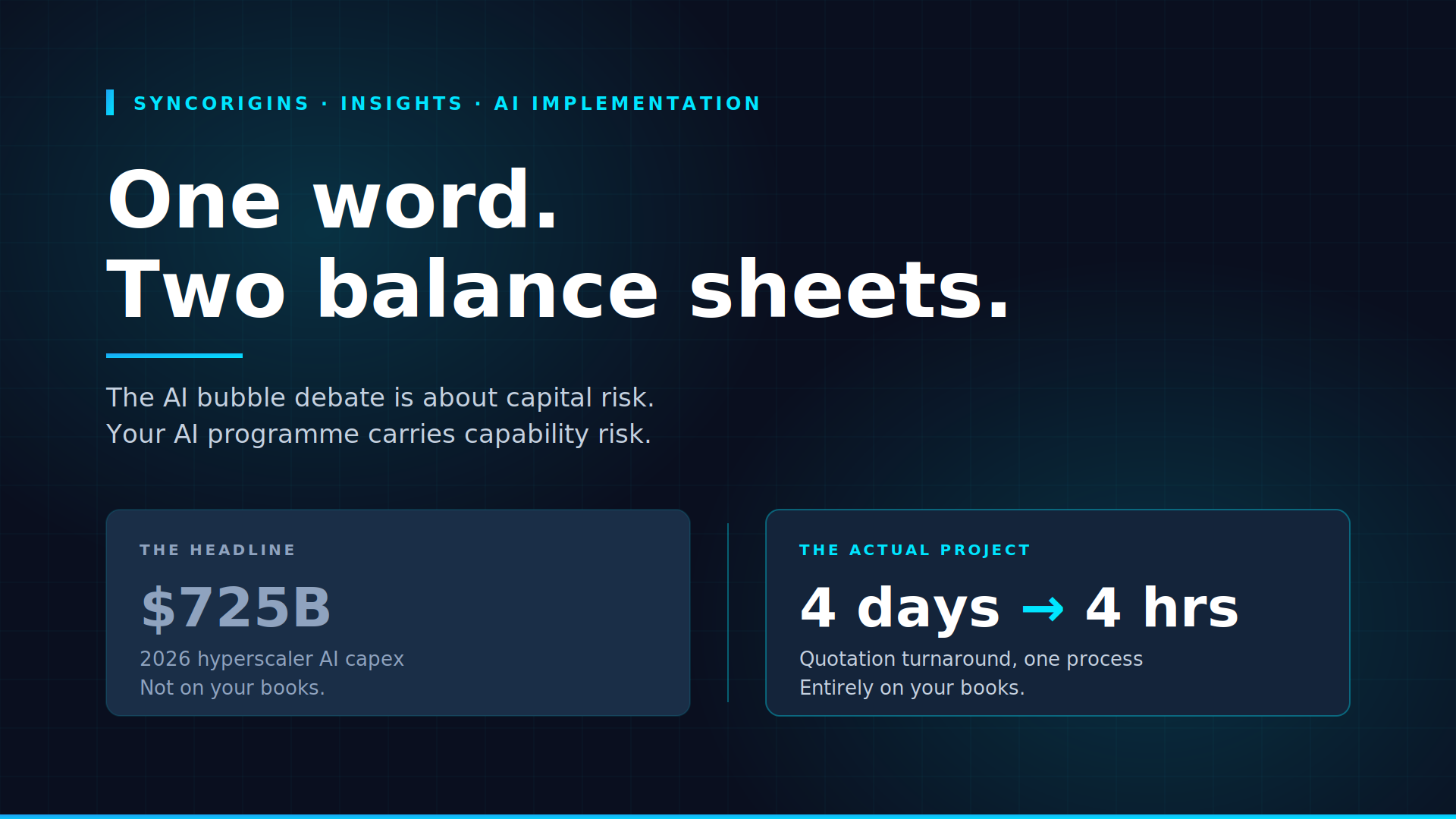

The COO of a £600M speciality manufacturer forwards a headline to her CTO on a Tuesday morning. Big Five hyperscaler capital expenditure, 2026: roughly $725 billion. Her note is three words long: “Should we pause?”

The AI programme she is asking about is a quotation agent. It reads inbound RFQs, pulls historical pricing and material availability, and drafts a quote for a human to approve. It would take her team’s turnaround from four days to under four hours on the two-thirds of enquiries that are routine. It has nothing whatsoever to do with data-centre construction, GPU depreciation schedules, or whether Alphabet’s capex guidance exceeds its operating cash flow.

She is not being irrational. She is making a category error — and it is the single most common one we encounter in mid-market AI conversations this year. The word “AI” in her headline and the word “AI” in her project charter refer to two entirely different things, carrying two entirely different risks, sitting on two entirely different balance sheets.

What the numbers actually say

Both halves of the argument are well evidenced, which is precisely why the debate is so confusing.

On the capital side, the scale is real. Combined 2026 capital expenditure for Amazon, Alphabet, Meta and Microsoft is projected at $700–750 billion, a 70–77% increase over 2025, with roughly three-quarters of it directed at AI hardware and infrastructure. Goldman Sachs projects cumulative hyperscaler investment exceeding $5.3 trillion by the end of 2030. Morgan Stanley and J.P. Morgan estimate the technology sector will need to issue around $1.5 trillion in new debt over three years to fund the build-out. Hyperscalers are now spending 45–57% of revenue on capex — ratios previously seen only in utilities and telcos.

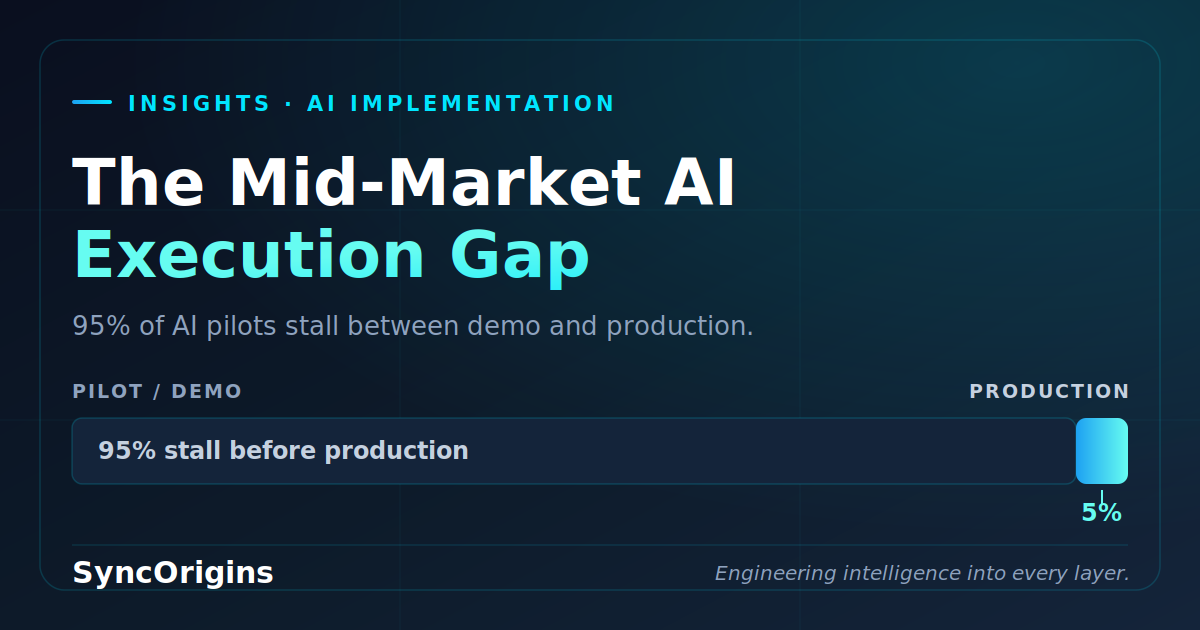

On the adoption side, the picture is equally stark but describes something else entirely. MIT’s Project NANDA research found roughly 95% of generative AI pilots delivered no measurable P&L return.

RAND reports that over 80% of AI projects fail to deliver intended business value — roughly twice the failure rate of comparable IT projects. Gartner forecasts that more than 40% of agentic AI projects will be cancelled by the end of 2027, and that 60% of AI projects unsupported by AI-ready data will be abandoned through 2026. S&P Global Market Intelligence found the average organisation scrapped 46% of its AI proofs-of-concept before production.

Read together, those two data sets are usually taken as one story: enormous money going in, nothing coming out, therefore bubble, therefore wait. That reading is wrong, and one further number from the same MIT research explains why.

Externally procured, narrowly scoped AI deployments succeeded roughly 67% of the time. Internally built general-purpose ones succeeded at around a third of that rate. The 95% failure figure is not a verdict on the technology. It is a verdict on how the work was scoped and bought.

| • | The infrastructure bubble. The question of whether $725 billion of annual data-centre and compute build-out will be matched by revenue on a timeline that justifies the debt used to fund it. This is a capital-markets risk borne by hyperscalers, their lenders and their shareholders. |

|---|---|

| • | The valuation bubble. The question of whether public-market prices for AI-exposed equities reflect earned profit or anticipated profit. This is a portfolio risk borne by investors. |

| • | The pilot bubble. The accumulation, inside ordinary companies, of AI proofs-of-concept that demonstrate capability without ever changing a process, a cost line or a revenue line. This is an operating risk, and it is the only one of the three you own. |

A correction would make your AI programme cheaper, not riskier

This is the part that gets lost. If you are a buyer of applied AI rather than an owner of AI infrastructure, your position in a correction is structurally different from a hyperscaler’s. You have no capex exposure, no depreciation schedule on two-to-three-year-life chips, and no debt raised against future inference revenue.

What a correction actually transfers to buyers is favourable: downward pressure on compute and model pricing, sharper competition among vendors chasing fewer buyers, and a loosening of the engineering talent market that has been the binding constraint on mid-market delivery for three years. The 2001 telecoms correction did not stop companies from using bandwidth. It made bandwidth cheap and made the firms that had built real applications on it very difficult to catch.

The genuine risk sits in the opposite direction. A company that pauses adoption for eighteen months does not avoid the pilot bubble — it simply arrives at the same starting line later, with less institutional data readiness, fewer people who have shipped anything, and competitors who spent the interval learning where AI actually holds in their workflows and where it doesn’t. Waiting is not a neutral position. It is a decision to acquire the same capability later, at a worse point on the learning curve.

None of which is an argument that AI spending is automatically sound. It is an argument that the bubble discourse is answering a question you were not asking.

How to build AI work that survives either outcome

If the capital-markets question is genuinely irrelevant to your programme, then the discipline that matters is the one that separates the 67% from the 95%. Six things do most of the work.

| 1. | Scope to a P&L line, not to a capability. “We want to use agentic AI” is not a scope. “We want quotation turnaround under four hours on routine RFQs, measured weekly” is. If nobody can name the line on the P&L that moves, the project has no owner and no stopping rule. |

|---|---|

| 2. | Fix the data path before the model. Gartner’s finding that 60% of projects without AI-ready data get abandoned is the single most actionable statistic in the field. The work of making pricing history, product master data and process records reliably queryable is unglamorous, and it is the majority of the effort. It also retains value regardless of which model you eventually run. |

| 3. | Buy narrow, build nothing generic. The success gap between externally procured, tightly scoped deployments and internal general-purpose platforms is roughly three to one. Build the thing that encodes your specific process. Buy or use off-the-shelf for everything that isn’t. |

| 4. | Set the abandonment date before you start. Fixed scope, fixed duration, defined success criteria agreed in writing at kick-off. A four-to-six-week proof with a stated kill condition is a decision-making instrument. An open-ended pilot is a way of avoiding a decision. |

| 5. | Keep the model layer replaceable. Abstract model calls behind your own interface from day one. Pricing shifts, vendors consolidate, and better models ship every few months. If a model change means a rewrite, you have coupled your business logic to a commodity that is actively repricing. |

| 6. | Instrument the workflow, not the demo. Measure the operational metric in production against a pre-agreed baseline, from week one. Demos are designed to succeed. The moment of truth is the first contact with real data, real exceptions and real users who have their own way of doing things. |

The honest version

We don’t know whether the market corrects. Nobody making that call publicly knows either, and the strength of the arguments on both sides is a fair indication that the answer isn’t currently knowable. That uncertainty is real and we won’t pretend otherwise.

What we would say with more confidence is that the answer doesn’t change the decision in front of most mid-market operators. A scoped agent that cuts quotation turnaround from four days to four hours is worth building if the numbers work, and not worth building if they don’t — and that arithmetic is unaffected by Alphabet’s financing structure.

And there is a version of this where pausing is the right answer. If you cannot name the process, the baseline metric and the person accountable for the outcome, then stopping is correct — but it was correct before anyone said the word “bubble”, and the bubble is not the reason. It is just the most respectable available excuse.

The companies that come out of this period ahead will not be the ones that predicted the capital cycle correctly. They will be the ones that shipped three narrow things that worked while everyone else was reading the headlines.